Module 6: ASEAN Legal Aspects

Table of Contents

Reading Text & Presentation

6.2.1 Free flow of skilled labor: seven professions and rules and regulations

INTRODUCTION What is the free flow? |

(Source: http://www.asean.org/communities/asean-economic-community retrieved 11/2/2014)

ASEAN Economic Community

The ASEAN Economic Community (AEC) shall be the goal of regional economic integration by 2015. AEC envisages the following key characteristics: (a) a single market and production base, (b) a highly competitive economic region, (c) a region of equitable economic development, and (d) a region fully integrated into the global economy.

The AEC areas of cooperation include human resources development and capacity building; recognition of professional qualifications; closer consultation on macroeconomic and financial policies; trade financing measures; enhanced infrastructure and communications connectivity; development of electronic transactions through e-ASEAN; integrating industries across the region to promote regional sourcing; and enhancing private sector involvement for the building of the AEC. In short, the AEC will transform ASEAN into a region with free movement of goods, services, investment, skilled labour, and freer flow of capital.

This module will focus on the free flow of skilled labour and the rules and regulations that are involved.

Free flow of skilled labour– Member countries are aiming to increase the mobility of labour within the ASEAN region, by facilitating the issuance of visas and employment passes for professionals and skilled labour, thus intensifying competition for employment opportunities in the region by 2015.

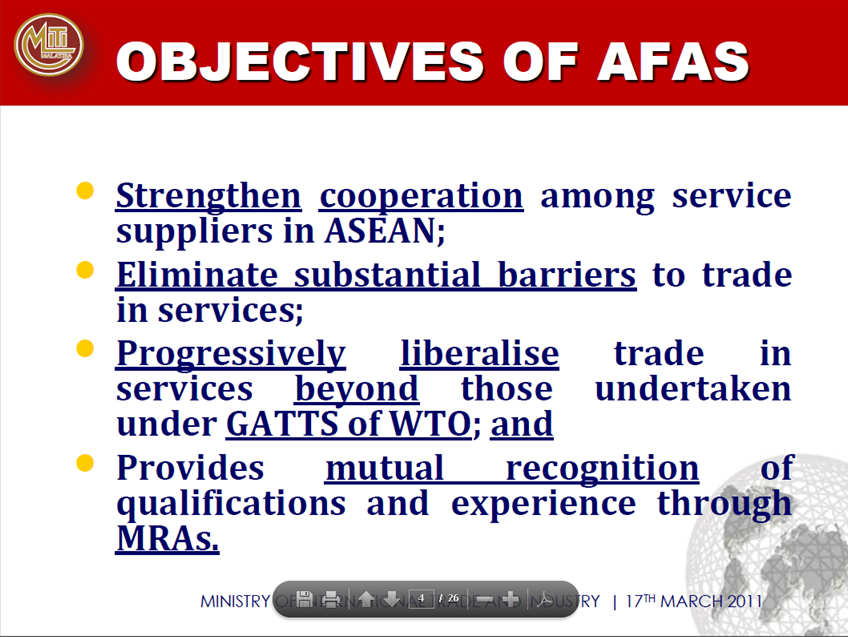

6.2.1 READING TEXT 1

Read the PowerPoint of the objective of the ASEAN framework agreement on services (Afas). This can give you the picture of rules and regulations that are involved with the free flow in ASEAN.

(Source: http://www.asean.org/communities/asean-socio-cultural-community/item/asean-framework-agreement-on-services-2

retrieved 11/2/2014)

(Source: http://www.mfea.org.my/Data/Sites/1/link/Announcement4/Afas.pdf retrieved 11/2/2014)

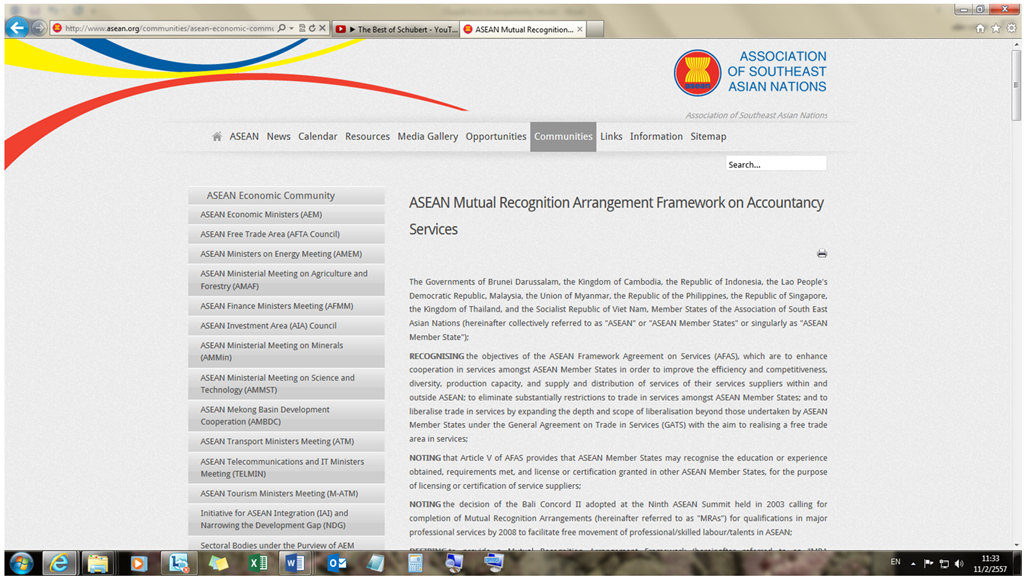

6.2.1 READING TEXT 2

The movement of professional-level labour in accordance with mutual recognition arrangements (MRAs).

(Source: http://www.asean.org/communities/asean-economic-community/item/asean-mutual-recognition-arrangement-framework-on-accountancy-services-3 retrieved 11/2/2014)

ASEAN Mutual Recognition Arrangement Framework on Accountancy Services

The Governments of Brunei Darussalam, the Kingdom of Cambodia, the Republic of Indonesia, the Lao People's Democratic Republic, Malaysia, the Union of Myanmar, the Republic of the Philippines, the Republic of Singapore, the Kingdom of Thailand, and the Socialist Republic of Viet Nam, Member States of the Association of South East Asian Nations (hereinafter collectively referred to as "ASEAN" or "ASEAN Member States" or singularly as "ASEAN Member State");

RECOGNISING the objectives of the ASEAN Framework Agreement on Services (AFAS), which are to enhance cooperation in services amongst ASEAN Member States in order to improve the efficiency and competitiveness, diversity, production capacity, and supply and distribution of services of their services suppliers within and outside ASEAN; to eliminate substantially restrictions to trade in services amongst ASEAN Member States; and to liberalise trade in services by expanding the depth and scope of liberalisation beyond those undertaken by ASEAN Member States under the General Agreement on Trade in Services (GATS) with the aim to realising a free trade area in services;

NOTING that Article V of AFAS provides that ASEAN Member States may recognise the education or experience obtained, requirements met, and license or certification granted in other ASEAN Member States, for the purpose of licensing or certification of service suppliers;

NOTING the decision of the Bali Concord II adopted at the Ninth ASEAN Summit held in 2003 calling for completion of Mutual Recognition Arrangements (hereinafter referred to as "MRAs") for qualifications in major professional services by 2008 to facilitate free movement of professional/skilled labour/talents in ASEAN;

DESIRING to provide a Mutual Recognition Arrangement Framework (hereinafter referred to as "MRA Framework") on Accountancy Services to facilitate the negotiations of MRAs in the Accountancy Services among ASEAN Member States as well as promoting the flow of relevant information and exchanging expertise, experiences and best practices suited to specific needs of each ASEAN Member State;

RECOGNISING the right of each ASEAN Member State to regulate the supply of the Accountancy Services sector within its territory;

NOTING the different levels of development of Accountancy Services among ASEAN Member States;

HAVE AGREED on this MRA Framework to encourage ASEAN Member States who are ready, to enter into bilateral or multilateral negotiations on MRAs on Accountancy Services.

ARTICLE I

ARTICLE II

In this MRA Framework, unless the context otherwise indicates:

ARTICLE III

ARTICLE IV

ARTICLE V

ARTICLE VII

For Brunei Darussalam:

|

Language Focus 6.2.1

Activities

Activity 11Activity 12Activity 13